The Decade Ahead in Seattle Multifamily: Why the Biggest Risk Is Also the Biggest Tailwind

The Puget Sound is about to run out of new apartments at precisely the moment the region makes it hardest to build or operate them. For investors with the right basis and the right submarket, that’s the setup.

For the next ten years, the Seattle multifamily thesis will be shaped by two forces pulling in opposite directions. One of them argues aggressively for getting capital into Puget Sound rental housing. The other argues for being deliberate about how and where you do it. The encouraging part is that both of them point toward the same conclusion: well-underwritten, well-located multifamily assets in the Seattle MSA are positioned to deliver some of the best risk-adjusted returns in U.S. commercial real estate over the next decade.

Let’s start with the tailwind, because it’s the one that matters most.

The Supply Cliff Is Already in the Pipeline

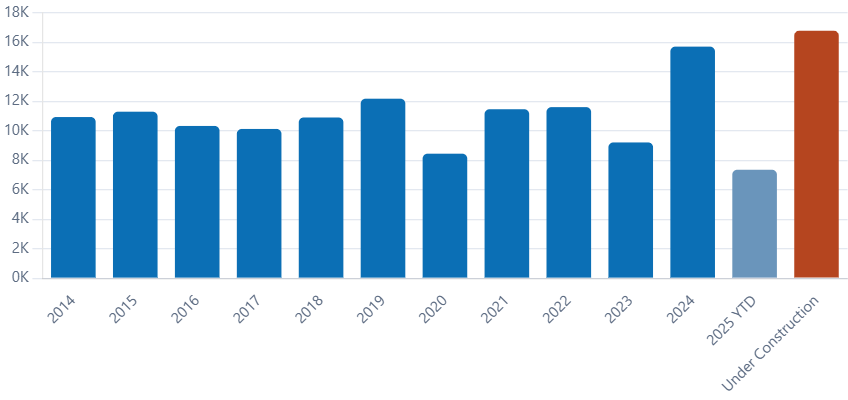

Puget Sound just came off one of its heaviest delivery years on record. More than 15,700 apartment units were completed across King, Snohomish, Pierce, and Kitsap counties in 2024 alone — roughly 50% above the ten-year average. Submarkets like South Lake Union, Capitol Hill, the Spring District, and downtown Bellevue absorbed thousands of units in short order, and concessions became a familiar sight. That era is ending fast. Starts fell off a cliff when the 10-year Treasury repriced construction economics. The roughly 16,800 units currently under construction across the four-county region will deliver over the next 24 to 36 months — which translates to annualized deliveries materially below what the region just absorbed in 2024.

Puget Sound Multifamily Deliveries & Forward Pipeline

Units delivered in King, Snohomish, Pierce & Kitsap counties (10+ unit buildings) vs. units currently under construction

Source: Kidder Mathews, 2025 Apartment Development Pipeline Report (Simon · Anderson Multifamily Team). 2025 figure is year-to-date at time of report publication. “Under Construction” represents the total current construction pipeline across the four-county region and will deliver over the following 24–36 months.

The absorption side of that equation is what makes it interesting. Amazon’s five-day return-to-office mandate has pulled tens of thousands of remote and hybrid workers back into the region. Microsoft continues to expand on the Eastside. Meta, Google, Salesforce, and a long tail of AI-adjacent companies are still hiring in Seattle and Bellevue. Boeing is stabilizing in Everett and Renton. Even as the headline tech narrative has cooled, the Seattle MSA is still adding jobs, and the center of gravity for both development and demand has quietly shifted east.

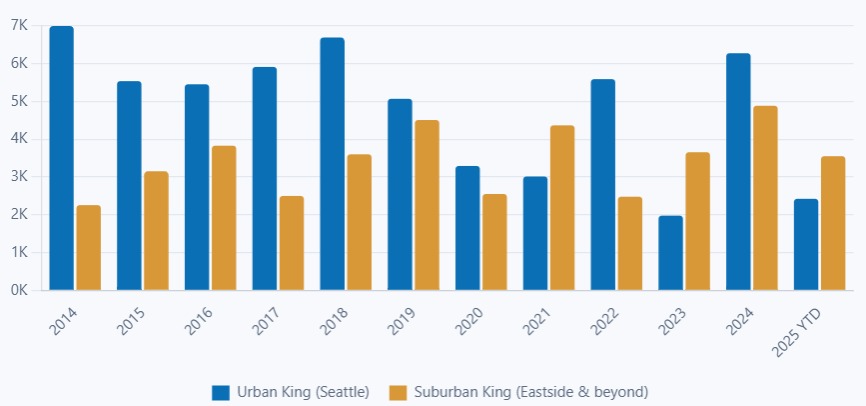

Development Has Shifted From Seattle to Suburban King

Apartment deliveries by year — Urban King (Seattle) vs. Suburban King (Eastside & beyond)

Source: Kidder Mathews, 2025 Apartment Development Pipeline Report (Simon · Anderson Multifamily Team). Since 2021, Suburban King has added 21,966 units versus 18,973 in Seattle — the first sustained inversion of the region’s development pattern.

Suburban King has led the region in deliveries every year since 2021, and its pipeline now outpaces the urban core by a wide margin.

The deeper point is structural. Even if interest rates cooperated tomorrow, the region couldn’t build its way out of the gap at anything close to the pace demand requires. Seattle design review regularly adds nine-to-twelve months to an entitlement timeline. SEPA appeals can stretch projects another year beyond that. Mandatory Housing Affordability (MHA) fees stack on top of permit and impact fees in most urban village zones. Tree protection ordinance revisions have narrowed what’s buildable on infill sites. In Bellevue, Kirkland, and Redmond, the entitlement process is friendlier but still measured in years, not months. By the time a project is shovel-ready in the Puget Sound, a competing project in Dallas has already leased up.

This is the upside case. Structural undersupply, a regulatory regime that actively slows the market’s ability to respond, and an employment base that keeps adding high-income renters — that is the foundation of a ten-year rental growth story. Existing stabilized stock is the scarce good. If you own it, you are long a resource the region is institutionally incapable of replacing at the pace that would relieve pressure on rents.

The Risk Is Political, Not Economic

Here is the other side of the ledger. The same political dynamic that makes building hard is increasingly being turned on the operators of existing assets. Washington’s 2025 passage of HB 1217 — the statewide rent-cap bill — was the watershed moment. For the first time, Washington capped annual residential rent increases (7% plus CPI, with hard ceilings on buildings over a certain age) across the entire state. A decade ago this was California’s problem. Today it’s Washington’s, and the direction of travel is unambiguous.

HB 1217 is not, on its own, catastrophic for a well-capitalized owner with a reasonable hold period and a sensible basis. What is concerning is the directional signal. Legislators in Olympia have discovered that rent control polls well even when its economic effects are widely understood to be counterproductive. The downside is asymmetric: a cap can be tightened in a single session, and once imposed, it is virtually never repealed. An asset you underwrote to 4% annual rent growth under one regulatory framework may be capped at something materially lower under the next one — and the equity math does not tolerate that kind of surprise.

A Decade of Seattle & Washington Housing Legislation

The cumulative operating environment has shifted materially in under ten years

Layered on top of state-level moves are the Seattle-specific operating costs: Rental Registration and Inspection Ordinance (RRIO) compliance, Economic Displacement Relocation Assistance, source-of-income protections, 180-day notice for rent increases over a threshold, security deposit caps, and application fee restrictions. Individually, these are manageable. Collectively, they shift risk and cost onto the owner in ways that were not priced into acquisitions underwritten in 2018 or 2019.

How to Hold Both Ideas at Once

The temptation is to read the two sections above and conclude that Seattle is a great market in theory and a minefield in practice. That is partly right, but it misses the bigger point. The legislative risk is itself a reason the supply-demand imbalance in the Seattle MSA is so durable. The same regulatory environment that makes owners nervous also keeps builders on the sidelines. The harder it is to raise rents, the harder it is to justify a new ground-up project — which means less competing supply, which means the existing rent roll on stabilized product gets more valuable, not less.

That dynamic is the mechanism. It is not an accident, and it is not priced in.

The trade in Seattle looks like this. First, be surgical about submarket. Eastside product (Bellevue, Kirkland, Redmond, Issaquah) and select Snohomish and Pierce submarkets offer a cleaner combination of job growth, entitlement functionality, and operating environment than much of the Seattle urban core — and the development data confirms capital is already voting with its feet. Suburban King County has 8,519 units under construction and another 43,667 in review, compared to 5,051 and 25,940 in Seattle (Kidder Mathews, 2025). Second, basis matters more than it did three years ago. Acquiring at or below replacement cost is the cleanest way to absorb a cap on future rent growth without destroying equity returns. Third, age matters: HB 1217’s tighter constraints on older product change the calculus on deep value-add plays, but they also reward well-located 2015–2022 vintage assets that sit above the older-asset cap threshold.

The Bottom Line

The Seattle MSA is entering a decade where the fundamentals favor owners of multifamily housing more decisively than they have in a generation. The chief risk is not cyclical — it is not rates, it is not a recession, and it is not overbuilding. It is a policy environment that is actively hostile to both the supply side and the operating side of the business. That risk is real, and it needs to be priced into every acquisition.

But the same policy environment is precisely what makes the Puget Sound supply gap so durable and the ownership position so valuable. This asset class is not getting less attractive in Seattle. It is getting more concentrated in the hands of operators who understand which submarkets to play, how to underwrite the political variable, and how to take advantage of the delivery trough that’s now locked in through 2027 and beyond. For investors, brokers, and owners thinking about the next ten years in the Puget Sound, that is the trade: get the submarket right, get the basis right, and let the imbalance do the work.